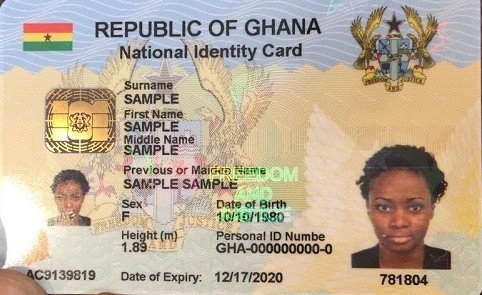

Ghana has rolled out payment functionality on its national ID cards, allowing millions of citizens to link bank accounts and carry out transactions using the Ghana Card, in a move aimed at accelerating financial inclusion and strengthening the country’s digital economy.

The development positions Ghana among a small group of countries globally integrating digital identity directly with financial services, a shift that could reshape access to banking not only domestically but across Africa as governments pursue similar models.

The initiative builds on earlier directives by the Bank of Ghana, which mandated the use of the Ghana Card for all financial transactions, laying the foundation for full identity-linked payments across the system.

Linking identity to finance

At the centre of the rollout is the National Identification Authority’s push to transform the Ghana Card from a verification tool into a multifunctional digital platform. The card, already widely used for SIM registration, tax identification, and banking verification, now serves as a gateway to financial services.

The system enables users to link their Ghana Card to bank accounts and payment platforms, allowing transactions without relying on debit cards or standalone mobile wallets. This reduces onboarding friction, particularly for individuals who lack additional forms of identification.

Infrastructure powering the system

The payments functionality is supported by Ghana’s national payments infrastructure, operated by the Ghana Interbank Payment and Settlement Systems (GhIPSS).

As the country’s central payment switch, GhIPSS enables interoperability between banks, fintech platforms, and government systems, ensuring that Ghana Card-linked transactions can be processed securely and efficiently.

This integration reflects a broader strategy to build sovereign financial infrastructure that reduces dependence on external payment networks while strengthening domestic digital capabilities.

The move is expected to expand access to financial services for millions of Ghanaians who remain unbanked or underbanked.

By using a single government-issued card, individuals can now perform transactions without navigating multiple financial platforms. This is particularly significant in rural and underserved areas, where access to banking services remains limited.

The biometric security features embedded in the Ghana Card enhance transaction safety, reducing fraud risks and improving trust in digital payments.

Impact on fintech and banking

The rollout is likely to deepen Ghana’s fintech ecosystem by increasing the number of users participating in formal financial networks. Banks and payment service providers stand to benefit from higher transaction volumes and improved customer acquisition.

It also creates new opportunities for innovation in areas such as digital lending, credit scoring, and insurance, as identity-linked financial data becomes more accessible.

As highlighted in Google Cloud powers Ecobank leap, Ghana’s financial sector has already been investing in advanced technologies to modernise banking services.

This momentum reflects wider continental trends outlined in Africa is building the future of fintech, where digital identity is increasingly central to scaling financial inclusion.

The integration of payments into the Ghana Card forms part of Ghana’s long-term ambition to build a fully interoperable digital economy anchored in secure identity systems.

Authorities have prioritised digital public infrastructure, including identity, payments interoperability, and regulatory frameworks to support fintech innovation.

These reforms are part of a wider policy direction captured in Ghana’s wider digital reform agenda, positioning the country as a regional leader in digital transformation and a potential model for other African economies.