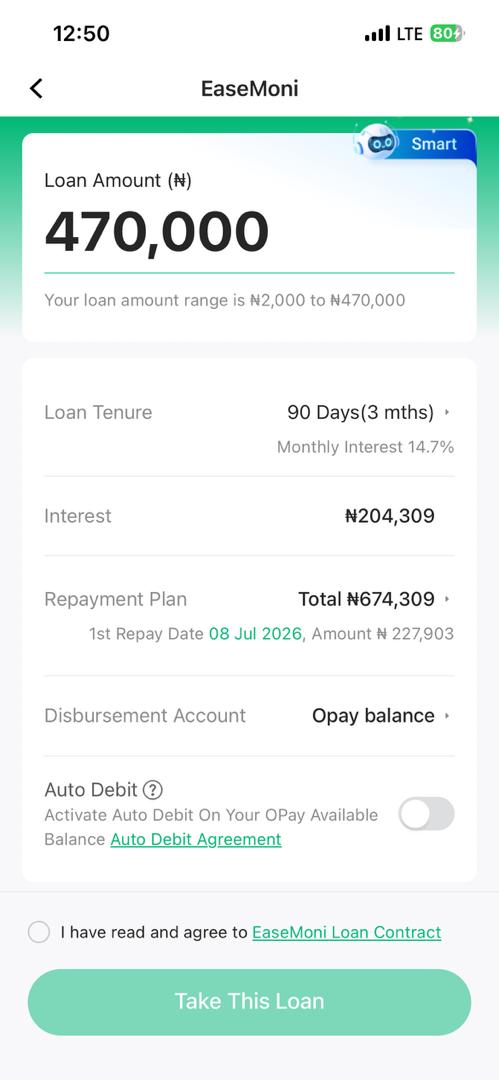

Nigerian borrower has publicly questioned the loan pricing practices of fintech company OPay after being charged ₦204,000 on a ₦470,000 loan, raising concerns about the effective interest rate applied to the facility.

In a post shared on social media platform X, the customer compared the loan charge with prevailing lending rates in Nigeria, arguing that the amount appeared significantly higher than what many commercial banks currently charge.

According to the borrower, Nigeria’s benchmark interest rate stands at 26.50 per cent, while some banks offer loans at rates of about 30 per cent annually.

The customer noted that a borrower taking a ₦100,000 loan at a 30 per cent annual rate would typically be expected to repay around ₦130,000 after one year.

Against that backdrop, the borrower questioned why a ₦470,000 loan attracted an additional ₦204,000 charge, which represents roughly 43 per cent of the principal amount.

“Dear OPay, why are you charging ₦204k on a ₦470k loan? That’s almost 50 per cent. Why?” the customer wrote.

The post has sparked discussion among social media users, with some calling for greater transparency in digital lending practices and clearer explanations of how interest rates, service charges, insurance fees and repayment structures are calculated.

Financial analysts note that the total cost of a loan may vary depending on factors such as the repayment period, risk assessment, administrative fees and other charges that lenders incorporate into their pricing models.

As of the time of filing this report, OPay had not publicly responded to the specific complaint.

The development highlights growing scrutiny of digital lending platforms as more Nigerians turn to fintech-powered credit services for personal and business financing amid challenging economic conditions.